Analyzing the Evolving Dynamics of Global Procurement Outsourcing Market Share

In the strategic world of business process outsourcing, the battle for Procurement Outsourcing Market Share is a contest between large-scale generalists and deep-domain specialists. The market share landscape is led by a group of large, global IT and BPO services giants, such as Accenture, IBM, and Capgemini. These companies command a significant share of the market by leveraging their vast global delivery networks, their long-standing relationships with large enterprise clients, and their ability to offer procurement outsourcing as part of a broader, integrated suite of finance and accounting services. Their strategy is to be the one-stop-shop for all of a company's back-office needs. This dominant position is, however, continuously challenged by a growing number of highly specialized, pure-play procurement service providers.

This strategic contest for market dominance is playing out within an industry that is growing at a strong and steady pace, providing opportunities for a range of players to succeed. The overall market is on a firm trajectory to expand to a size of USD 10.47 billion by 2032, propelled by a healthy compound annual growth rate (CAGR) of 13.70%. This sustained growth means that while the large BPO giants are powerful, there is ample room for the specialized providers to capture significant market share. These smaller, more agile firms often win business by offering deeper category expertise, more flexible engagement models, and more advanced, purpose-built technology platforms than their larger, more generalized competitors, creating a dynamic and competitive environment.

The primary strategies for capturing market share are varied. For the large BPO players, the key strategy is to bundle services and leverage their scale to offer a cost-competitive, end-to-end solution. They often win large, multi-year contracts by integrating procurement services with other outsourced functions like finance and HR. In contrast, the specialized providers win market share by positioning themselves as true strategic partners with deep expertise. They often focus on a specific industry vertical or a complex spend category, and they compete on the quality of their insights and the tangible savings they can deliver. A major strategic battleground is technology, with market share being won by the providers who can offer the most powerful and user-friendly platforms for spend analytics and e-sourcing.

Looking forward, the future distribution of market share will likely be shaped by the ability to deliver technology-enabled services and to cater to the growing mid-market. As clients demand more automation and data-driven insights, the providers who have invested in building or acquiring advanced technology platforms powered by AI and machine learning will have a significant competitive advantage. Furthermore, as procurement outsourcing becomes more accessible to medium-sized enterprises, the providers who can offer a more flexible, scalable, and cost-effective service model will be well-positioned to capture this large and underserved segment of the market, potentially reshaping the market share landscape in the coming years.

Explore Our Latest Trending Reports:

Категории

Больше

The latest business intelligence report released by Polaris Market Research on Tangential Flow Filtration Market Size, Share, Trends, Industry Analysis Report By Product (Single-use Tangential Flow Filtration Systems, Reusable Tangential Flow Filtration Systems), By Technology, By Application, By End Use, By Region – Market Forecast, 2025–2034. It covers the in-depth knowledge...

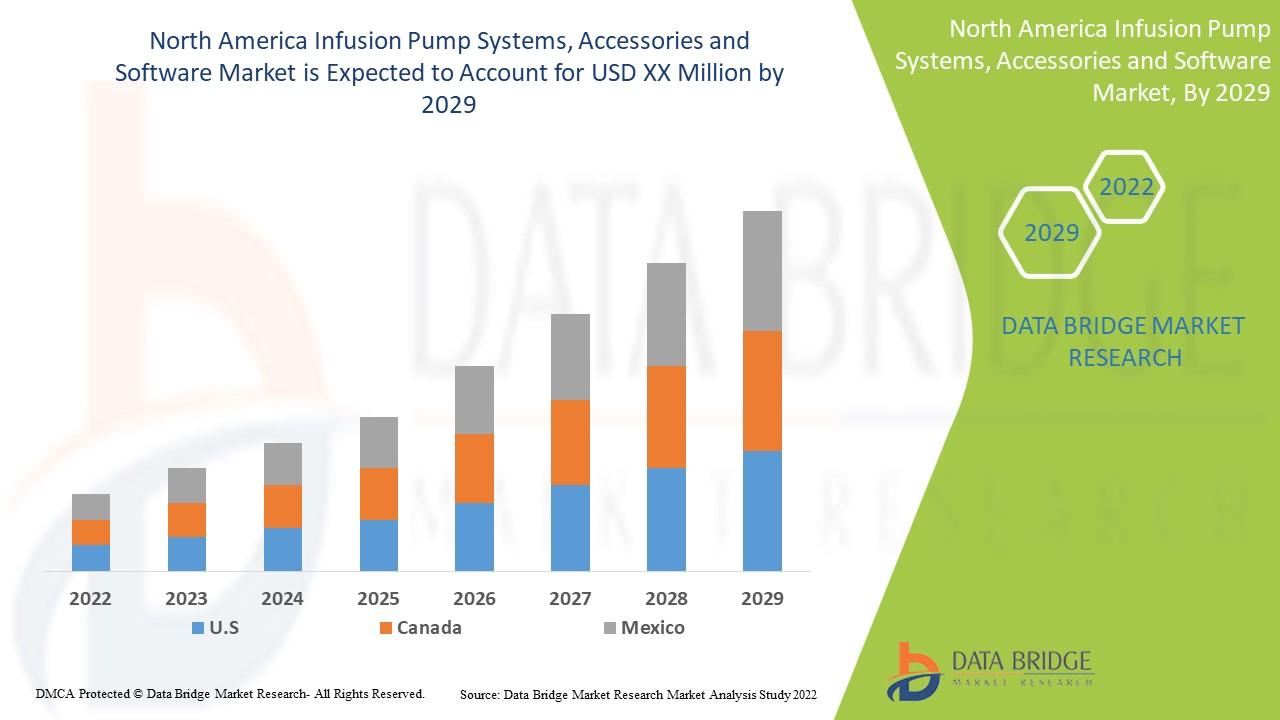

"Executive Summary: North America Infusion Pump Systems, Accessories and Software Market Size and Share by Application & Industry Data Bridge Market Research analyses that North America infusion pump systems, accessories and software market will grow at a CAGR of 11.1% during the forecast period of 2022 to 2029. A worldwide North America Infusion Pump Systems, Accessories...

When searching for reliable construction and landscaping equipment, the Mini Dumper Factory offers innovative solutions for transporting heavy loads efficiently, even in confined or uneven spaces. These compact machines have become essential tools for contractors, landscapers, and urban maintenance teams looking for performance, mobility, and safety. Traditional methods of moving construction...

The top executive looked at the quarterly report with a confused look on their face. The figures didn’t make sense. Even though they were trying hard to minimize costs and were in talks with several suppliers, spending had nonetheless gone up by 8% over the previous year. Departments were buying things from dozens of suppliers, some of whom they had never heard of before. The IT staff...

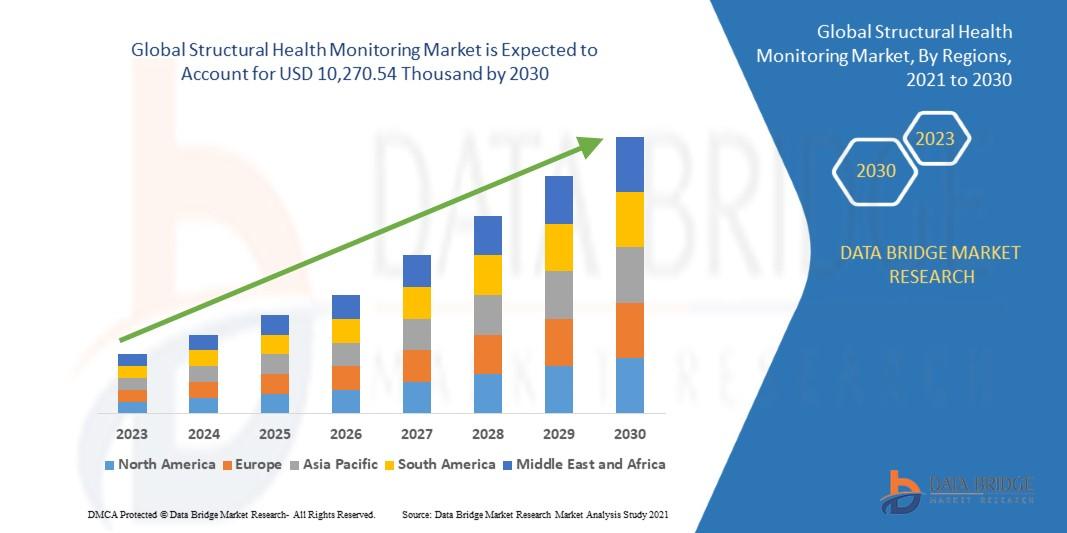

"Executive Summary Structural Health Monitoring Market Research: Share and Size Intelligence CAGR Value Data Bridge Market Research analyzes that the global structural health monitoring market is expected to reach the value of USD 10,270.54 thousand by 2030, at a CAGR of 17.9% during the forecast period. The large scale Structural Health Monitoring Market report gives explanation...