Navigating the Competitive 3D Simulation Software Market

The global 3D Simulation Software Market is a highly sophisticated and intensely competitive arena, dominated by a mix of established engineering software giants and highly specialized niche players. This dynamic landscape is driven by the insatiable demand from industries seeking to accelerate innovation, reduce development costs, and improve product quality through virtual testing. The significant financial stakes involved are fueling constant M&A activity and R&D investment, as vendors vie for dominance in a market set for exponential growth. A recent analysis projects the market's value will reach a remarkable USD 33.87 Billion by 2034, a trajectory powered by a powerful compound annual growth rate of 17.20% from 2025. This rapid expansion underscores the fierce competition among providers to deliver the most accurate, comprehensive, and user-friendly simulation solutions available to a diverse industrial clientele.

At the top of the competitive hierarchy are the large, diversified engineering software conglomerates. Companies like Dassault Systèmes (with its SIMULIA and SOLIDWORKS brands), Siemens (Simcenter), and Autodesk are major players, offering 3D simulation as a key component of their broader product lifecycle management (PLM) and computer-aided design (CAD) ecosystems. Their primary competitive advantage lies in their ability to offer a deeply integrated, end-to-end solution where design, simulation, and manufacturing data flow seamlessly. These industry titans leverage their extensive global sales channels, large existing customer bases, and significant R&D budgets to maintain a commanding market position, particularly within large enterprise accounts that prioritize platform consolidation and a single-vendor relationship for their entire engineering software stack, making them formidable competitors in the market.

Challenging the dominance of these integrated suite providers is a vibrant ecosystem of specialized, best-of-breed vendors. Companies like Ansys and Altair have built their entire businesses around providing deep, high-fidelity simulation capabilities across a wide range of physics disciplines, including structural analysis, computational fluid dynamics (CFD), and electromagnetics. Their key differentiator is the depth and accuracy of their solvers and their reputation as the "gold standard" for complex engineering challenges. These specialized players often appeal to R&D departments and simulation experts who require the highest level of precision and are willing to manage a multi-vendor software environment to get it. This focus on deep scientific expertise allows them to maintain a strong and loyal customer base, particularly in research-intensive industries like aerospace, defense, and high-performance automotive sectors.

The future of competition in the 3D simulation market will be defined by several key trends. The move towards the cloud is a major battleground, with vendors racing to offer flexible, scalable, and powerful simulation capabilities via a Software-as-a-Service (SaaS) model. This democratizes access to high-performance computing, allowing smaller companies to tackle complex simulations that were previously out of reach. Another critical area of competition is the integration of artificial intelligence (AI) and machine learning to accelerate simulation times and enable generative design, where the software autonomously explores thousands of design variations to find the optimal solution. The vendors who can most effectively harness these trends to make simulation faster, more accessible, and more intelligent will be best positioned to lead this rapidly evolving and highly lucrative market.

Explore Our Latest Trending Reports:

Catégories

Lire la suite

The consumer goods industry is always a reflection of global consumption habits, driven significantly by lifestyle, personal spending, and evolving preferences. No matter the cycles in external influences, the global Hair Color Market overall long-term performance tends to be stable. From 2025 to 2032, total growth will be at a cagr of 6.5% from 2025 to 2032, and valuation will increase in sync...

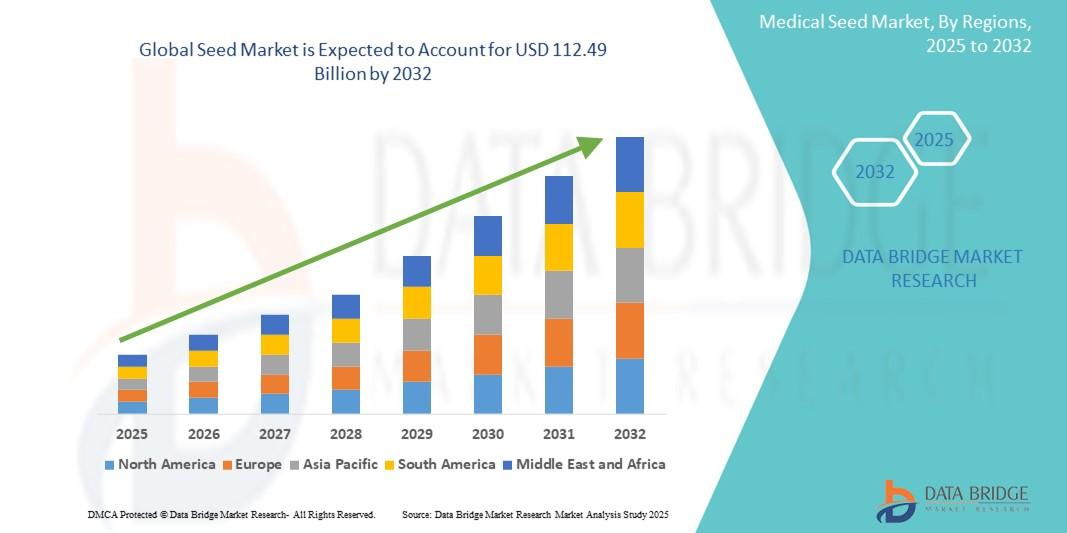

"Regional Overview of Executive Summary Seed Market by Size and Share CAGR Value The global seed market size was valued at USD 61.68 billion in 2024 and is expected to reach USD 112.49 billion by 2032, at a CAGR of 7.80% during the forecast period. With the superior Seed Market report, get knowledge about the industry which explains what market...

"Detailed Analysis of Executive Summary Paprika Powder Market Size and Share CAGR Value The global paprika powder market size was valued at USD 5.86 billion in 2024 and is expected to reach USD 9.84 billion by 2032, at a CAGR of 6.7% during the forecast period. An international Paprika Powder Market research report is planned by gathering market research...

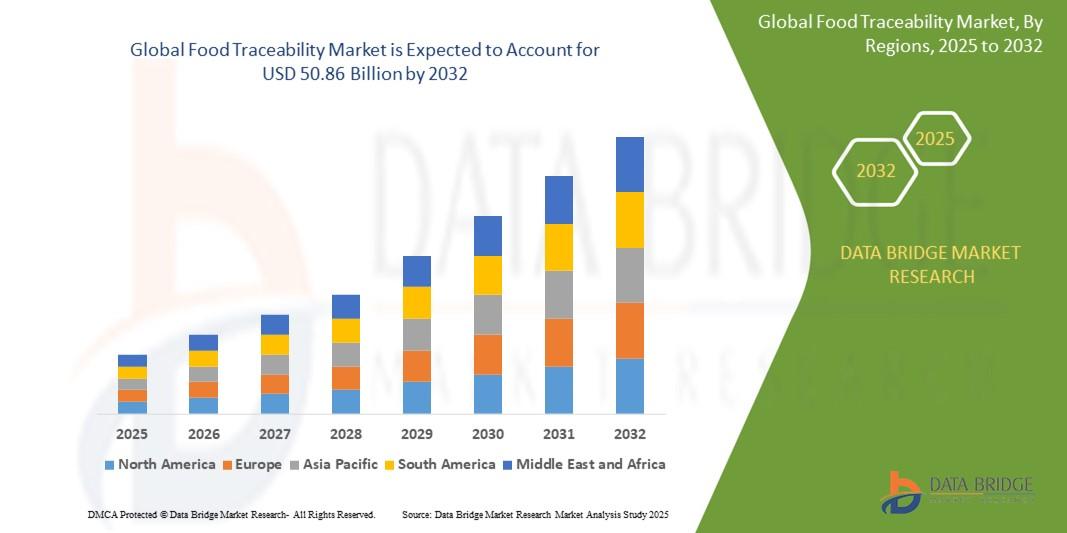

"Executive Summary Food Traceability Market Size and Share Forecast CAGR Value The global food traceability market size was valued at USD 23.21 billion in 2024 and is expected to reach USD 50.86 billion by 2032, at a CAGR of 10.30% during the forecast period. Complex market insights are represented in a simpler version in the world class Food Traceability...

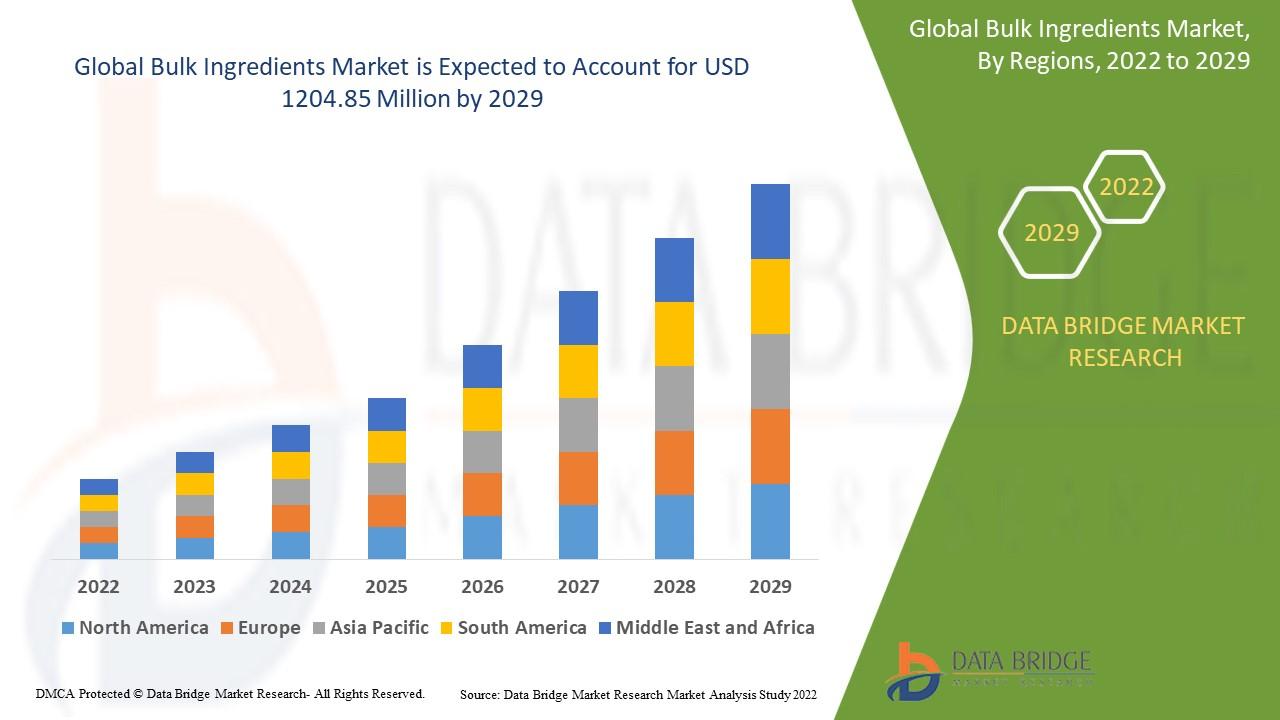

Introduction The Global Bulk Ingredients Market plays a vital role in sustaining multiple industries, including food and beverages, pharmaceuticals, cosmetics, and personal care. Bulk ingredients refer to raw materials such as grains, sweeteners, oils, chemicals, minerals, and additives that serve as the foundation for finished products. Their large-scale production and supply ensure...