North America Optical Transport Market Witnesses Rapid Upgrades in High-Speed Networking Systems

North America Optical Transport Market Overview

The North America Optical Transport Market is witnessing strong growth as enterprises, hyperscale data centers, telecom operators, and cloud service providers rapidly upgrade their network infrastructures to support massive data consumption. The surge in high-speed internet demand, expansion of 5G networks, rising cloud adoption, and growing need for data center interconnect (DCI) solutions are fueling adoption across the region. Optical transport technologies—particularly WDM, DWDM, ROADM, and packet-optical transport systems—are now core enablers of low-latency, high-bandwidth communication required for modern digital services. As industries embrace digital transformation, optical transport systems are essential for supporting applications such as IoT, AI-driven analytics, edge computing, UHD video streaming, and enterprise cloud workloads. The market is characterized by rapid innovation, significant investments in fiber infrastructure, and strong demand for scalable, energy-efficient, and automated optical networking solutions. With the rise of bandwidth-hungry applications and the shift toward open optical networking architectures, the North America region remains one of the most dynamic and technologically advanced markets globally.

Market Key Players

Major companies operating in the North America Optical Transport Market include Ciena Corporation, Cisco Systems, Nokia, Huawei Technologies (limited presence due to regulatory restrictions), Infinera Corporation, Fujitsu Network Communications, ADVA Optical Networking, ZTE Corporation, and NEC Corporation. These players focus heavily on R&D to enhance network capacity, introduce open optical and disaggregated networking solutions, and integrate advanced automation capabilities. Ciena and Infinera lead in coherent optical technologies, while Cisco and Nokia dominate in integrated IP-optical platforms used by telecom operators and cloud providers. Strategic partnerships, product launches, and network upgrade deals with large carriers like AT&T, Verizon, T-Mobile, and major data center operators further drive market advancements. The players also compete through AI-driven network optimization tools, 800G/1.2T coherent optics, and green networking solutions that reduce power consumption across large-scale optical infrastructure.

Market Segmentation

The North America Optical Transport Market is segmented based on technology, component, data rate, application, and end-user. By technology, the market includes Wavelength Division Multiplexing (WDM), Dense WDM (DWDM), Coarse WDM (CWDM), and Optical Transport Network (OTN) solutions. By component, the market comprises optical fibers, optical amplifiers, transceivers, wavelength selective switches, and multiplexers/demultiplexers. Based on data rates, the market spans 100G, 200G, 400G, 600G, 800G, and emerging 1.2T coherent optical technologies. Key applications include long-haul networks, metro networks, data center interconnect (DCI), 5G fronthaul and backhaul, and cloud interconnection. End-users include telecom service providers, cloud providers, enterprises, BFSI, government agencies, and media & entertainment companies. The rapid migration toward higher-capacity 400G and 800G solutions, combined with open line systems, is reshaping segmentation patterns across the region.

Market Drivers

The market is primarily driven by the exponential growth in data traffic generated from video streaming, cloud computing, IoT ecosystems, and digital platforms. The rollout and expansion of 5G networks across North America significantly increase the need for high-capacity optical transport to support low-latency and high-bandwidth backhaul connections. Massive cloud migration and the rising number of hyperscale data centers further push demand for fast, reliable DCI solutions. Enterprises across industries are adopting automation, AI, and analytics, creating the need for advanced optical networks that can handle large-scale data flows. The shift toward 400G and 800G coherent optics is accelerating due to the demand for higher throughput and enhanced spectral efficiency. Another major driver is the push for open and disaggregated optical networking, which enables cost-effective scaling and vendor flexibility. Government investments in broadband expansion and fiber deployment programs also strengthen market growth.

Market Opportunities

Significant opportunities emerge from the rapid expansion of edge computing, which requires distributed high-capacity optical connectivity across regional locations. Growing adoption of 5G standalone networks opens new prospects for optical fronthaul and midhaul solutions. The increasing volume of AI and machine learning workloads at data centers drives demand for ultra-high-speed optical connectivity and integration of advanced coherent optical modules. Green networking is becoming a major opportunity as enterprises and operators aim to reduce energy consumption, creating demand for energy-efficient transport systems. There is strong potential in rural fiber rollout programs, network modernization initiatives by enterprises, and the shift from legacy TDM platforms to fully packet-based optical networks. Open optical networking architectures—including open ROADM and white-box optical line systems—offer opportunities for innovation and cost optimization. As cybersecurity threats increase, secure optical transport solutions with encryption and enhanced visibility tools also present new growth avenues.

Regional Analysis

The United States dominates the North America Optical Transport Market due to strong investments by telecom operators, hyperscale cloud providers, and enterprises involved in digital transformation. Major carriers such as AT&T, Verizon, and Lumen Technologies continuously upgrade backbone networks with DWDM and 800G coherent solutions to handle massive data traffic. The presence of major cloud players—including Google, Amazon Web Services, Microsoft, Meta, and Oracle—creates significant demand for high-capacity data center connectivity, especially across inter-city and metro networks. Canada is experiencing steady growth driven by nationwide broadband expansion programs, 5G deployment initiatives, and rising cloud adoption among enterprises and government agencies. Canadian telecom operators like Bell Canada and Rogers Communications are actively investing in optical transport upgrades. Mexico is also emerging as a growth market with increasing investments in fiber-optic infrastructure and expanding demand for advanced network services. Overall, North America remains a global leader in optical networking technology, benefiting from strong digital investments, regulatory support, and continuous innovation.

Industry Updates

The optical transport industry in North America is witnessing rapid innovation, particularly in coherent optical technologies, open networking, and automation. Recent industry updates highlight large-scale deployments of 800G and 1.2T coherent solutions by leading carriers, enabling them to handle rising data demands with higher spectral efficiency. Network operators are increasingly adopting open line systems to enhance interoperability and reduce vendor lock-in. Several players have introduced AI-powered optical network management tools that provide predictive analytics, automated fault detection, and real-time performance optimization. Mergers and partnerships between technology vendors and cloud providers continue to accelerate network modernization efforts. Data center operators across the region are upgrading DCI infrastructures with advanced ROADM-based architectures to ensure scalability and low-latency connectivity. Sustainability is becoming a core focus, with companies introducing energy-efficient optical modules and low-power network equipment to meet ESG goals.

Categorie

Leggi tutto

The Marine Engine Market Analysis is undergoing significant transformation as the global maritime industry embraces cleaner, more efficient, and technologically advanced propulsion systems. As per Market Research Future, the market is witnessing strong growth driven by rising international trade, fleet modernization, and stringent environmental regulations. Marine engines—responsible for...

A new growth forecast report titled Fresh Food Packaging Market Size, Share, Trends, Industry Analysis Report By Material, By Pack Type, By Application, and By Region – Market Forecast, 2025–2034 introduced by Polaris Market Research represents conclusive data on the overall market. It majorly targets to provide a detailed analysis of growth factors, challenges, and...

Executive Summary Automotive Heating, Ventilation, and Air Conditioning (HVAC) Market Research: Share and Size Intelligence CAGR Value Data Bridge Market Research analyses that the automotive heating, ventilation, and air conditioning (HVAC) market is expected to reach USD 48.56 billion by 2030, which is USD 22.49 billion in 2022, at a CAGR of 10.10% during the forecast period....

The Virtual Desktop Market Trends are shaping the way organizations adopt flexible and secure computing environments. With increasing demand for VDI solution and remote desktop environment technologies, businesses are transitioning to cloud desktop platforms and virtual workstations to support distributed workforces. The growth of enterprise desktop virtualization is enabling IT teams to...

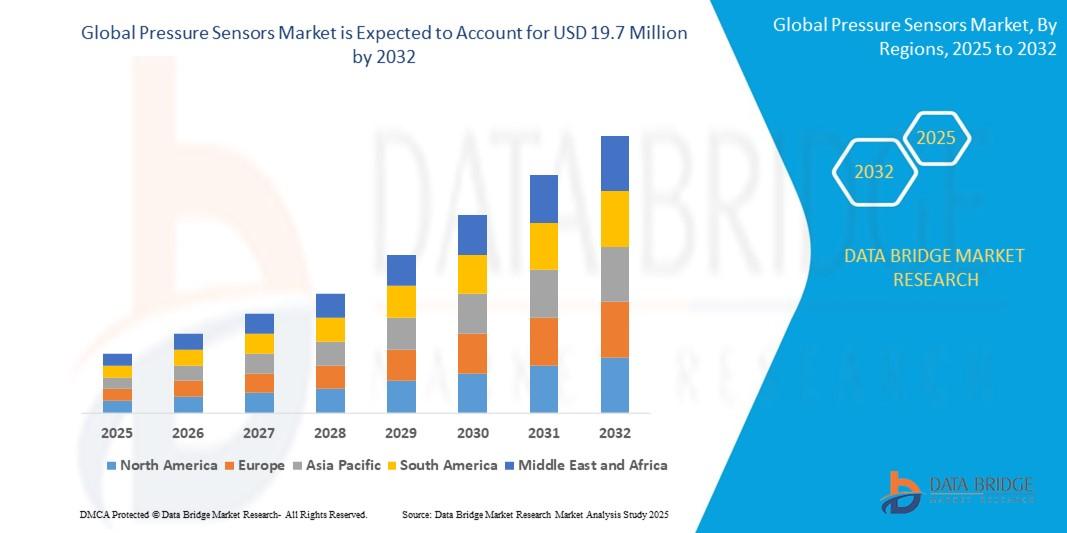

"Global Demand Outlook for Executive Summary Pressure Sensors Market Size and Share The Global Pressure Sensors Market size was valued at USD 12.1 Million in 2024 and is expected to reach USD 19.7 Million by 2032, at a CAGR of 7.2% during the forecast period Pressure Sensors Market report supports businesses to thrive in the market by providing them with an array...