Electric Vehicle Battery Charger Market Share Gains Momentum in Electrified Mobility Era

The global market for Electric Vehicle Battery Charger Market is entering a new phase of rapid growth as electric mobility becomes mainstream and charging infrastructure expands globally. For a deeper dive into this evolving sector, check out the full report here: Electric Vehicle Battery Charger Market Share Report. What was once a supplementary accessory is now a critical component of the electrified vehicle ecosystem—and its market share is climbing accordingly.

Market Share Drivers

The rise in market share for EV battery chargers is driven by two broad forces: the surge in electric-vehicle ownership and the demand for more advanced charging systems. As more consumers and fleets adopt EVs, they require more charging stations, more efficient charger hardware, smarter software, and services around charging. This growth means the charger segment is capturing a larger proportion of value in the overall electric-vehicle system.

Policy and regulatory support play a key role. Countries worldwide are setting ambitious zero-emission targets, setting deadlines for phasing out internal-combustion vehicles, and rolling out financial incentives for EV buyers and charging-station installation. This creates momentum behind charging-infrastructure investment and elevates the charger market’s share. At the same time, automotive manufacturers are designing vehicles with higher voltage systems (400 V, 800 V), faster charging capability and built-in compatibility with smart chargers—all of which raises the per-unit value of charger hardware and boosts its share.

Trends Shaping the Market Share Landscape

Several important trends are reshaping how the charger market share evolves. First, the shift from slow and standard home chargers toward high-power fast and ultra-fast chargers is transformative. Vehicles capable of 800 V systems, fleets that need rapid turnaround, and highway hubs all demand chargers that are larger, smarter and costlier—raising the overall value of the charger market.

Second, software and connectivity are becoming intrinsic. Chargers aren’t just boxes anymore—they’re network-connected, cloud-enabled, capable of load-management, billing, and integrating with energy-systems and grid-services. As these added capabilities grow, the charger market captures more of the value chain and thus more share.

Third, regional dynamics are shaping share. For instance, the Asia-Pacific region continues to lead in volume of EVs, installations of chargers, and manufacturing of charger hardware. Meanwhile, Europe and North America drive value via premium equipment, smart infrastructure, and services. As emerging markets ramp up, they will drive further share expansion globally.

Lastly, the aftermarket and service segments are becoming more meaningful. As charging networks age, require upgrades, maintenance, software updates, and enhancements, the ancillary market around chargers expands—and this also contributes to market-share growth beyond new installations.

Regional Insights

In volume terms, Asia-Pacific holds a dominant share due to its large EV adoption and installation programmes. Countries like China and India are rapidly scaling charger infrastructure, which helps the charger market share in units. Europe and North America meanwhile contribute high-value equipment and premium systems, which lift the share in value terms. As infrastructure build-out accelerates globally, the charger market share is expected to broaden geographically.

Challenges and Opportunities for Further Share Growth

The future upside for charger market share is substantial—but there are some challenges. One is the cost and complexity of high-power charger deployment, including grid-connection, site acquisition, permitting, and standards. Another is the fragmentation of standards and connectors—ensuring compatibility remains important. Supply-chain risks—semiconductors, power electronics, cables—also apply. Despite these hurdles, the opportunities are compelling: ultrafast chargers, commercial and fleet charging, subscription and software-based charging services, vehicle-to-grid integration, and growing adoption in emerging markets. Charger hardware and network providers aligned with these opportunities will secure a larger slice of the market share.

Looking Ahead: Share Trajectory

Looking forward, the charger market share will continue to expand—in both units and value per unit. As vehicles offer longer range, higher voltages, faster charge capability, the requirements on chargers increase—and thus charger system value goes up. Firms that invest in advanced hardware (e.g., 350 kW+ chargers), modular architecture, software connectivity, global reach and service models will capture the lion’s share. For investors, infrastructure developers, automakers and service providers, the time to engage is now.

In summary, the electric-vehicle battery charger market is no longer a peripheral niche—it’s a core component of the electrified mobility ecosystem. Its share of the mobility value chain is rapidly increasing as EV adoption accelerates, charging technology advances and infrastructure scales. For stakeholders in electrified mobility—from charger manufacturers and network operators to automakers and charging service providers—the opportunity to shape and capture this market is here.

More Related Report

Automotive Connecting Rod Market Size

Categorii

Citeste mai mult

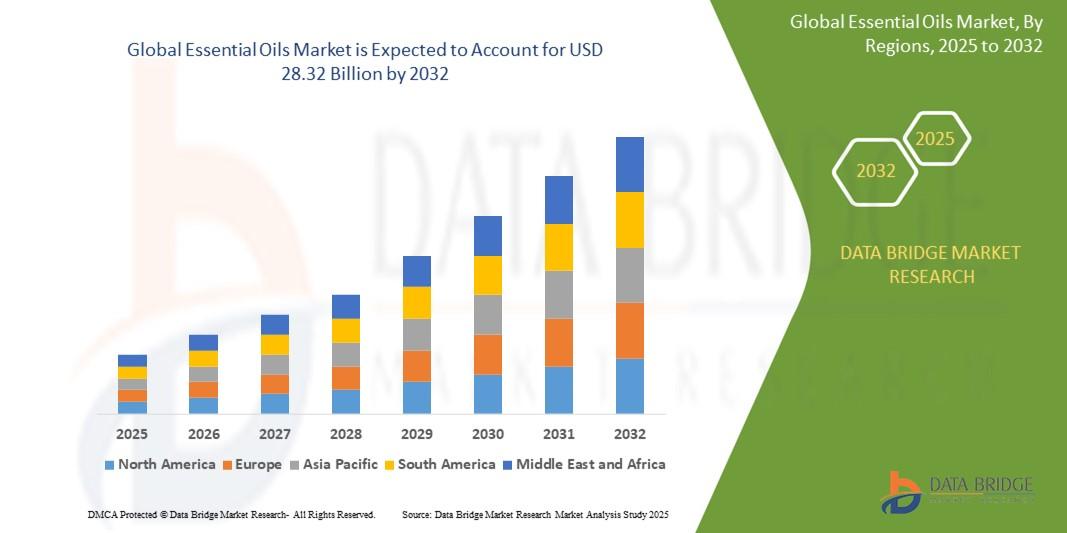

「エグゼクティブサマリーエッセンシャルオイル市場の将来:規模とシェアのダイナミクス」 CAGR値 世界のエッセンシャルオイル市場は 2024年に171億8000万米ドルと評価され 、 2032年までに283億2000万米ドルに達すると予想されています。2025年から2032年の予測期間中、市場は 主に消費者の天然製品への嗜好の高まりにより、6.5%のCAGRで成長すると見込まれています 。 この成長は、アロマセラピーや代替医療の成長、ウェルネスやクリーンラベルのトレンドへの移行などの要因によって推進されています。...

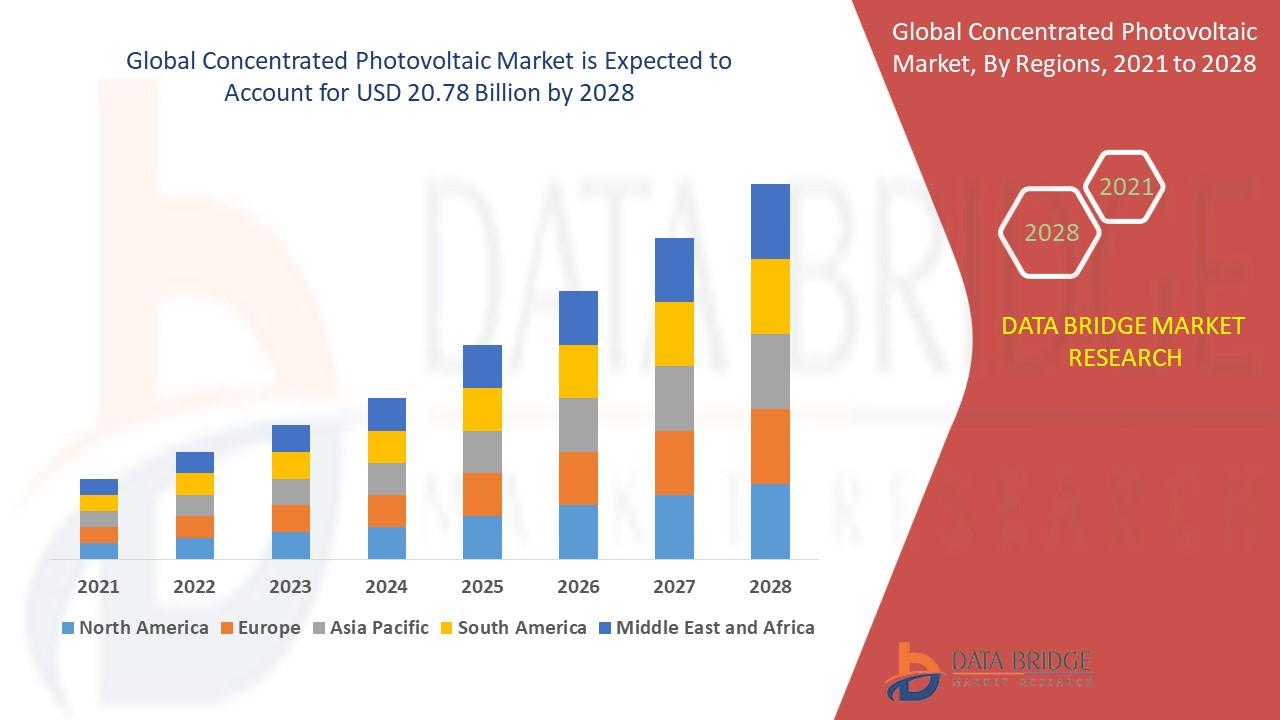

"Regional Overview of Executive Summary Concentrated Photovoltaic Market by Size and Share Concentrated photovoltaic market size is valued at USD 20.78 billion by 2028 and is expected to grow at a compound annual growth rate of 21.70% for the forecast period of 2021 to 2028. A study about the Concentrated Photovoltaic Market overview is performed by considering market drivers, market...

The future of the Nordic plastic packaging film market appears promising, driven by innovation, sustainability, and evolving consumer demands. Countries in the region, including Denmark, Sweden, Norway, and Finland, are actively pursuing environmental responsibility through strict regulations, circular economy initiatives, and incentives for sustainable packaging solutions. These factors are...

The Hybrid Storage Arrays Market share is increasingly defined by a mix of established vendors and emerging players competing to provide high-performance, scalable storage solutions. Hybrid Storage Arrays Market Size was valued at 8.6 USD Billion in 2024. The Hybrid Storage Arrays Market is projected to grow from 9.31 USD Billion in 2025 to 20.5 USD Billion by 2035, representing a CAGR of...

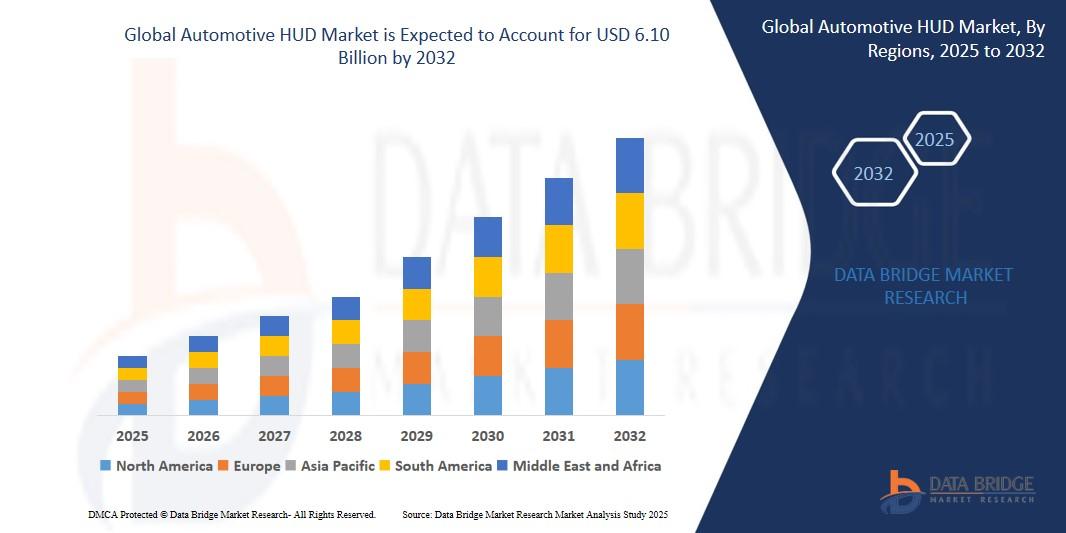

"Executive Summary Automotive HUD Market Value, Size, Share and Projections CAGR Value The Global Automotive HUD Market size was valued at USD 1.74 billion in 2024 and is expected to reach USD 6.10 billion by 2032, at a CAGR of 19.9% during the forecast period. Being a comprehensive in nature, Automotive HUD Market report undeniably meets the strategic...