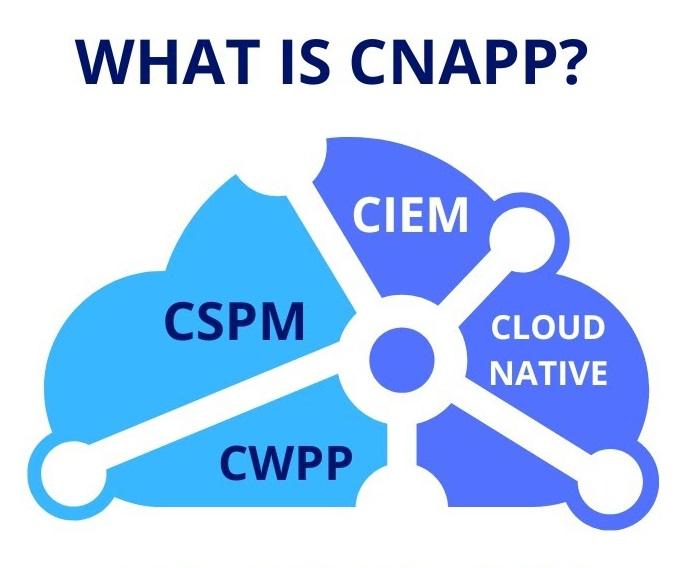

Analyzing the Competitive Dynamics of CNAPP Market Share Distribution

The fierce competition for Cloud-native Application Protection Platform Market Share has created a dynamic and rapidly consolidating landscape. The enormous potential of this sector, which is forecast to become a $71.92 billion industry by 2035, has attracted a diverse array of competitors, all vying for a dominant position. This impressive market size will be realized through a robust growth rate of 21.72% from 2025 to 2035, making it one of the most hotly contested battlegrounds in all of cybersecurity. The ongoing struggle for market share is characterized by rapid innovation, aggressive go-to-market strategies, and a significant wave of mergers and acquisitions as larger players look to build out comprehensive platform offerings. Understanding these competitive dynamics is key to anticipating the future direction of the market and the evolution of cloud security technology.

The battle for market share is being fought on several fronts. One major group of competitors consists of the major public cloud providers themselves: Amazon Web Services (AWS), Microsoft Azure, and Google Cloud Platform (GCP). These hyperscalers are increasingly offering their own suite of native security tools (e.g., AWS Security Hub, Microsoft Defender for Cloud) that provide foundational CNAPP capabilities. They leverage their incumbent position and deep integration with their own platforms as a key advantage, offering a convenient, single-vendor solution for customers who are primarily on one cloud. Their strategy is to make their native tools the default choice, capturing market share by bundling security directly with their core cloud services, which poses a significant competitive challenge to third-party vendors.

On the other side are the pure-play cybersecurity vendors and established security platform companies. This group includes industry giants like Palo Alto Networks, CrowdStrike, and Fortinet, who have leveraged their strong brand recognition, large enterprise customer bases, and extensive sales channels to enter the CNAPP market. Their strategy often involves acquiring best-of-breed CNAPP startups and integrating them into their broader security platforms, offering customers a single solution for endpoint, network, and cloud security. This "platformization" approach appeals to large enterprises looking to consolidate their security vendors and simplify their security operations. They compete by offering deeper security expertise and more advanced threat detection capabilities than the native cloud provider tools, positioning themselves as the premium, comprehensive security partner for multi-cloud environments.

A third, and highly influential, group shaping market share consists of the venture-backed, cloud-native startups. Companies like Wiz, Orca Security, and Lacework have disrupted the market with innovative, agentless architectures and a relentless focus on user experience. Their agentless approach simplifies deployment and provides broad visibility across an organization's entire cloud estate within minutes, a compelling value proposition that has allowed them to rapidly acquire customers and significant market share. Their strategy is to out-innovate the larger, more established players with superior technology and a more intuitive, developer-friendly product. The success of these startups has triggered a wave of high-profile acquisitions, demonstrating that innovation from smaller players is a primary driver shaping the long-term distribution of market share.

Explore Our Latest Trending Reports:

Categorias

Leia Mais

A thorough Insulated Wire Cable Market Analysis reveals how evolving infrastructure priorities are dictating capital flows, M&A activity, and product innovations across the sector. Market Size was valued at 33.1 USD Billion in 2024 and is projected to reach 50 USD Billion by 2035, with a CAGR of 3.8%. Segment analysis points to rapid expansion in optical fiber and...

Methyl acetate is steadily becoming a critical solvent in industries that demand both high performance and environmental compliance. Its fast evaporation rate and pleasant odor make it a superior alternative to harsher solvents traditionally used in paints, adhesives, and packaging inks. As sustainability drives packaging innovation, methyl acetate’s role as a biodegradable and low-VOC...

"Executive Summary: Europe Orthopedic Implants Market Size and Share by Application & Industry CAGR Value The Europe orthopedic implants market size was valued at USD 19.54 billion in 2024 and is expected to reach USD 52.32 billion by 2032, at a CAGR of 13.10% during the forecast period A worldwide Europe Orthopedic Implants Market report comprises of...

Polaris Market Research has introduced the latest market research report titled Viral Vector Manufacturing Market Share, Size, Trends, Industry Analysis Report, By Vector Type; By Workflow; By Application; By End-Use; By Region; Segment Forecast, 2021 - 2028 that highlights the major revenue stream for the forecast period. The report contains clear, reliable, and thorough Viral Vector...

The nanofilms market is rapidly transforming the energy storage and electronics sectors, offering solutions that improve efficiency, longevity, and performance. These ultrathin films, often just a few nanometers thick, provide critical functionality in batteries, supercapacitors, and solar cells. In energy storage, nanofilms enable higher charge density, faster ion transport, and enhanced...