The Key Players: Mapping the Global Geospatial Market Share

The competitive battle for Geospatial Market Share is a dynamic contest featuring a mix of long-established software giants, major aerospace and defense contractors, and a new wave of agile satellite imagery providers. The landscape is complex, with different companies dominating different layers of the geospatial technology stack, from data acquisition to software analytics. As the market continues to expand and become more mainstream, the competition to become the go-to provider for location intelligence is intensifying. The enormous value of this market is why the competition is so fierce, with the total Geospatial Market is Estimated to Reach a Valuation of USD 274.41 Million By 2035, Reaching at a CAGR of 9.12% During 2025 - 2035.

In the crucial GIS and spatial analytics software segment, the market share has long been dominated by Esri (Environmental Systems Research Institute). With its comprehensive ArcGIS platform, Esri has a commanding presence in government, utilities, and academia, built on decades of deep functionality and a strong user community. It faces competition from other major software players like Hexagon, which offers a broad portfolio of geospatial and industrial enterprise solutions, and Trimble, which has a strong position in surveying, construction, and agriculture. A growing open-source software ecosystem, with tools like QGIS, also holds a significant "mindshare," particularly in academia and among individual users, providing a powerful and free alternative to commercial software.

In the Earth Observation and satellite imagery segment, the market share landscape has been dramatically reshaped in recent years. For decades, the market was dominated by a few large satellite operators like Maxar Technologies and Airbus. However, a new generation of companies, most notably Planet, has disrupted the market by deploying massive constellations of small, relatively inexpensive satellites. This allows them to image the entire Earth every single day, a feat previously unimaginable. This "NewSpace" approach has shifted the business model from selling individual, high-resolution images to selling a subscription-based data feed, and has dramatically increased the volume and timeliness of available imagery, creating a new competitive dynamic.

The strategy for gaining market share in this evolving industry is increasingly focused on platforms and cloud delivery. Instead of just selling raw data or a standalone desktop software product, the leading companies are building integrated, cloud-based platforms that combine data, software, and analytics in a single offering. Esri's ArcGIS Online, Maxar's SecureWatch, and Planet's Explorer are all examples of this trend. By offering their solutions as a service on the cloud, companies can make their technology more accessible, scalable, and easier to integrate into their customers' existing workflows. The battle for market share is no longer just about having the best sensor or the best algorithm; it's about providing the most powerful and user-friendly platform for turning geospatial data into answers.

Kategoriler

Read More

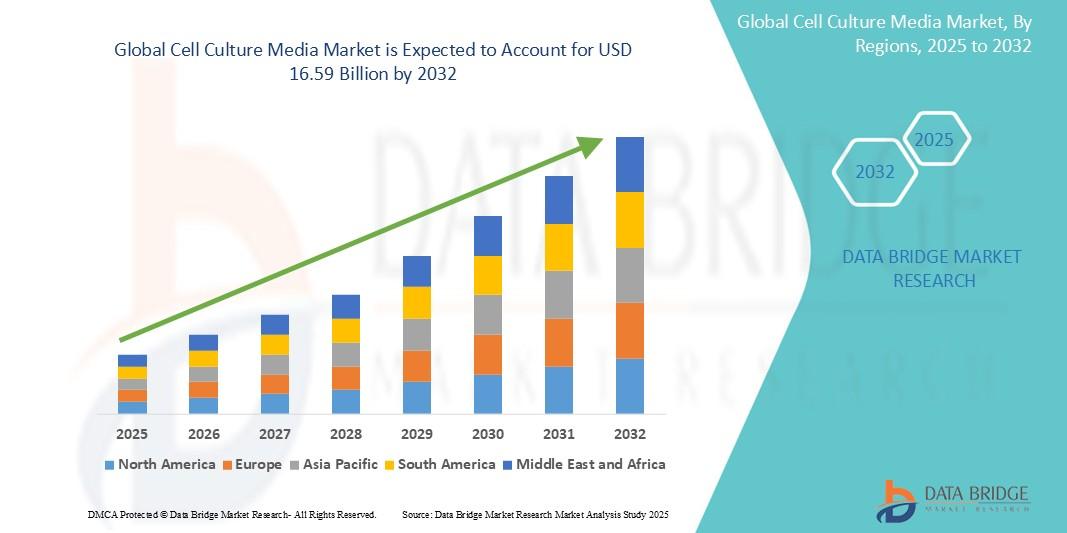

Executive Summary The Global Cell Culture Media Market has emerged as a critical segment of the biotechnology and life sciences industry, underpinning advancements in biopharmaceuticals, regenerative medicine, vaccine development, and translational research. Driven by rising demand for innovative therapies and increasing investments in research and development, the market has seen...

"Market Trends Shaping Executive Summary Hospital Staffing Market Size and Share CAGR Value The global hospital staffing market size was valued at USD 40.50 billion in 2024 and is expected to reach USD 65.68 billion by 2032, at a CAGR of 6.23% during the forecast period. An extensive market research report like Hospital Staffing Market report...

As per MarkNtel Advisors The India Makhana Market size is valued at around USD 1.46 billion in 2025 and is expected to reach USD 2.23 billion by 2030. Along with this, the market is estimated to grow at a CAGR of around 8.80% during the forecast period, i.e., 2026-30 India Makhana Market Systems Market Outlook: The Russian Seed Market is rapidly evolving, driven by agricultural...

The global Law Firm market leads the nation's so-called 'renaissance', such that each industrial segment is endowed with well-efficient and networked solutions. IT infrastructure forms a necessity, ranging from cloud storage to cybersecurity. Based on market performance during 2024-2031, the sector experiences a CAGR of 1.7%, whereas valuation continues to provide proof of the...

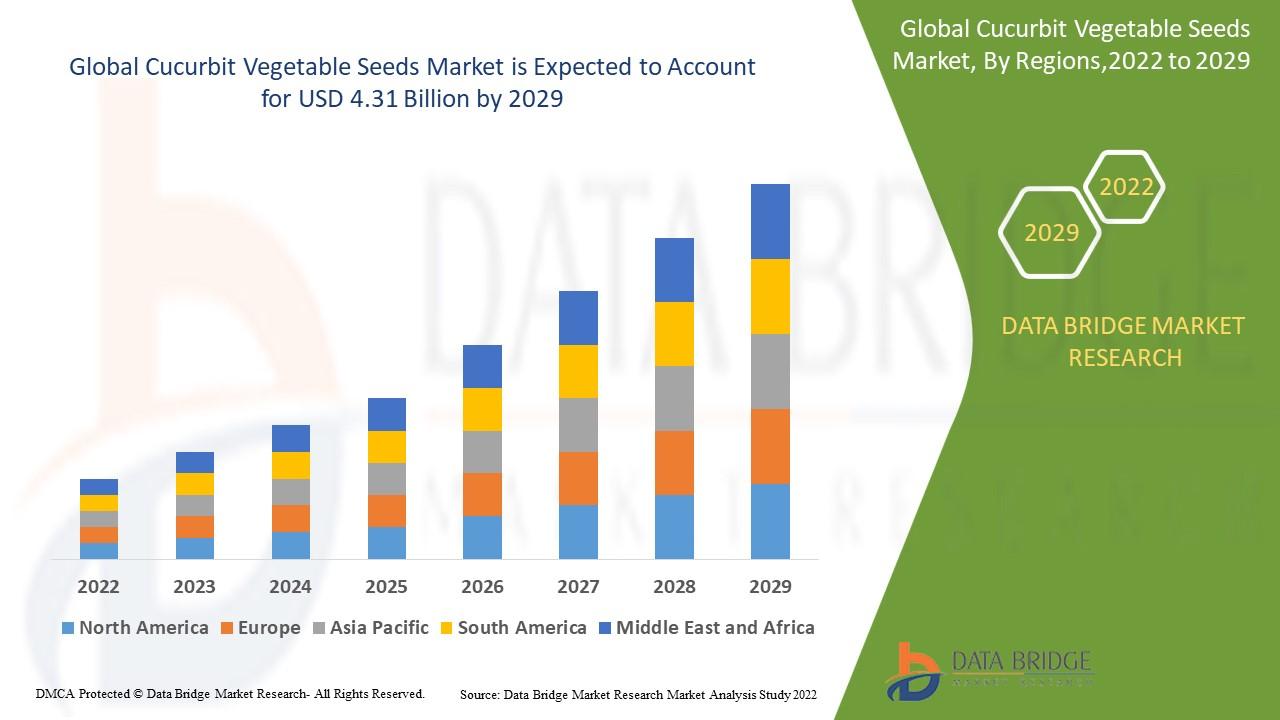

Introduction The Global Cucurbit Vegetable Seeds Market represents one of the most dynamic segments within the agricultural seed industry. Cucurbit vegetables, including cucumbers, pumpkins, melons, gourds, squashes, and zucchinis, are widely cultivated across diverse climatic regions. These crops hold immense economic importance as they form a staple part of human diets worldwide and...