Testing Inspection and Certification (TIC) Market Size, Drivers, and Key Players

Despite its strong growth trajectory, the Testing, Inspection, and Certification industry is not immune to challenges that can hinder its progress and impact its profitability. A realistic assessment must carefully consider the Testing Inspection and Certification (TIC) Market Restraints that players in this sector must navigate. One of the most significant and persistent restraints is the lack of globally harmonized standards and regulations. While there has been progress in some areas, many product categories are still subject to a patchwork of different national and regional technical requirements. For a manufacturer wishing to sell a product globally, this means having to undergo multiple, often redundant, sets of tests and certifications to meet the specific requirements of each market. This regulatory fragmentation increases costs and complexity for businesses and can act as a technical barrier to trade. For TIC companies, it means they must invest in maintaining accreditations and expertise for a wide variety of different standards, which can be inefficient and costly. While this complexity can also be a driver of business, it simultaneously acts as a structural restraint on the overall efficiency and seamless functioning of the global market.

Another major restraint is the perpetual challenge of finding, training, and retaining a highly skilled workforce. The TIC industry relies on the deep technical expertise of its engineers, chemists, auditors, and inspectors. These professionals require a unique combination of scientific knowledge, analytical skills, and unwavering integrity. As products and regulations become more complex, the demand for specialists in niche fields like cybersecurity, functional safety, or specific types of medical device testing is growing rapidly. However, the supply of qualified talent often struggles to keep pace, leading to a "war for talent" that can drive up labor costs and create operational bottlenecks. The need for continuous training to keep staff updated on the latest technologies, standards, and testing methodologies adds another layer of cost and complexity. This human capital constraint is a critical operational risk for TIC companies and can limit their ability to scale up and capitalize on new market opportunities, particularly in highly specialized or emerging fields.

Finally, the industry faces the dual restraints of high capital investment and the constant threat of commoditization. Setting up and maintaining a network of state-of-the-art accredited laboratories requires a massive and ongoing capital expenditure. Sophisticated testing equipment is expensive to purchase, calibrate, and maintain. This high capital barrier can make it difficult for new players to enter the market and compete with established giants. At the same time, in mature segments of the market where testing procedures are well-established and standardized, services can become commoditized, leading to intense price competition and eroding profit margins. This forces companies into a difficult balancing act: they must continuously invest heavily in high-tech, high-margin areas to stay ahead of the curve, while simultaneously fighting to maintain profitability in their high-volume, commoditized service lines through operational efficiency and automation. The risk of fraudulent certificates and the need to invest in digital security to protect the integrity of their reports also represent a growing financial and reputational burden, acting as another significant restraint on the industry.

Categorieën

Read More

The market for goods and services supplied to publicly funded educational institutions is characterized by a unique and resilient growth dynamic. The Government Education CAGR (Compound Annual Growth Rate), while perhaps not as explosive as some high-tech sectors, is notable for its stability, predictability, and immense scale. This steady growth is fundamentally underpinned by the...

"Latest Insights on Executive Summary Asia-Pacific Orthobiologics Market Market Share and Size CAGR Value The Asia-Pacific Orthobiologics Market was valued at USD 1.8 Billion in 2024 and is expected to reach USD 2.68 Billion by 2032, at a CAGR of 5.1% during the forecast period. Asia-Pacific Orthobiologics Market Market report presents...

Zusammenfassung: Größe und Marktanteil des Parfümmarktes nach Anwendung und Branche CAGR-Wert Der globale Parfümmarkt hatte im Jahr 2024 ein Volumen von 54,01 Milliarden US-Dollar und dürfte bis 2032 ein Volumen von 74,49 Milliarden US-Dollar erreichen , was einer jährlichen Wachstumsrate von 4,10 % im...

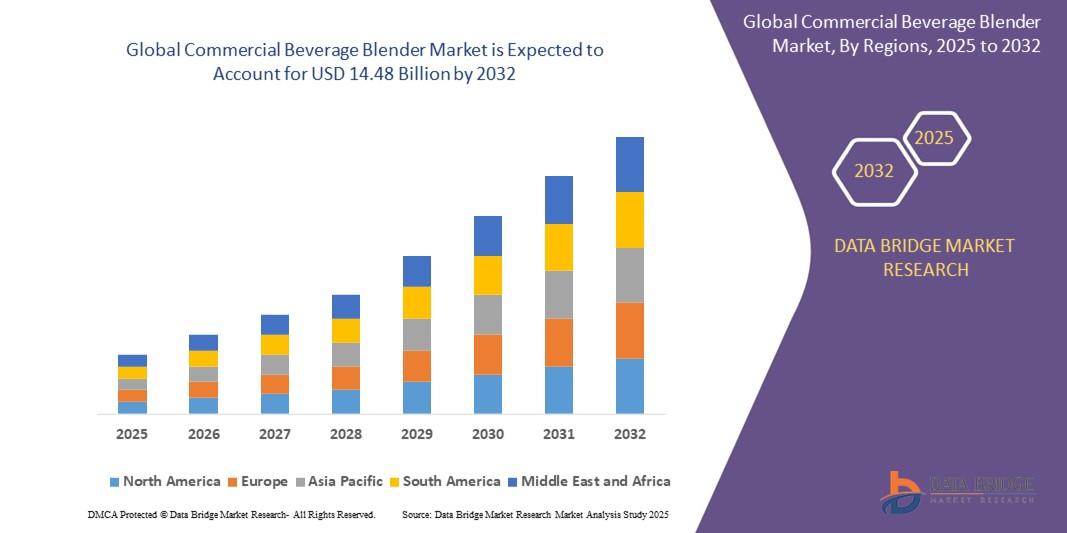

"Executive Summary Commercial Beverage Blender Market Market Size, Share, and Competitive Landscape CAGR Value The global commercial beverage blender market size was valued at USD 10.88 billion in 2024 and is expected to reach USD 14.48 billion by 2032, at a CAGR of 3.64% during the forecast period. This Commercial Beverage Blender Market...

The US Wholesale Telecom Market size reflects significant expansion opportunities as enterprises increasingly require high-capacity and reliable communication services. Valued at USD 436.77 billion in 2023, the market is projected to reach USD 1,167.07 billion by 2032, growing at a CAGR of 11.54% from 2024 to 2032. The increasing need for cloud adoption, managed services, and high-speed...