The Competitive Landscape of Global Geospatial Market Share

The global competition for Geospatial Market Share is a dynamic and multifaceted contest involving a diverse range of companies, from established software giants to innovative satellite operators and agile service providers. This rivalry is for dominance in a market that is expanding at a healthy pace, with forecasts showing it will grow to a valuation of USD 274.41 million by 2035, driven by a steady 9.12% CAGR. In this environment, market share is captured by offering a combination of powerful technology, high-quality data, deep industry expertise, and a strong ecosystem of partners and developers. The landscape is a fascinating mix of platform dominance, data supremacy, and specialized service excellence.

The market share landscape for GIS software is heavily dominated by Esri, whose ArcGIS platform is the de facto standard in many government agencies, universities, and large corporations. Its comprehensive feature set, strong brand reputation, and massive user community give it a powerful and entrenched market position. Other major players in the broader geospatial software and hardware space include Hexagon, Trimble, and Autodesk, each with strongholds in specific industries like construction, surveying, and engineering. These companies compete by offering end-to-end solutions that often combine their own specialized hardware and software to provide a complete workflow for their target customers.

In the crucial data segment of the market, the competition for market share is among the satellite imagery providers. Companies like Maxar Technologies, Planet Labs, and Airbus operate constellations of Earth observation satellites, competing to provide the highest resolution, most frequently updated, and most comprehensive global imagery. Their customers range from government intelligence agencies to agricultural technology companies. The rise of numerous smaller "NewSpace" companies launching their own satellite constellations is increasing competition and driving down the price of data, making it accessible to a wider range of users and fueling market growth.

The future distribution of market share will be heavily influenced by the rise of cloud computing and AI. The major public cloud providers—Amazon Web Services (AWS), Microsoft Azure, and Google Cloud—are becoming major players in the geospatial market. They are not only offering the scalable infrastructure needed to process massive geospatial datasets but are also providing their own native geospatial services and AI tools. This is creating a new competitive dynamic, where traditional geospatial vendors are both partnering with and competing against the cloud giants. The companies that can best leverage the power of the cloud and AI to deliver easy-to-use, scalable, and insightful solutions will be the ones to win the future battle for market share.

Explore Our Latest Regional Trending Reports!

Spain Direct Carrier Billing (DCB) Market

Categories

Read More

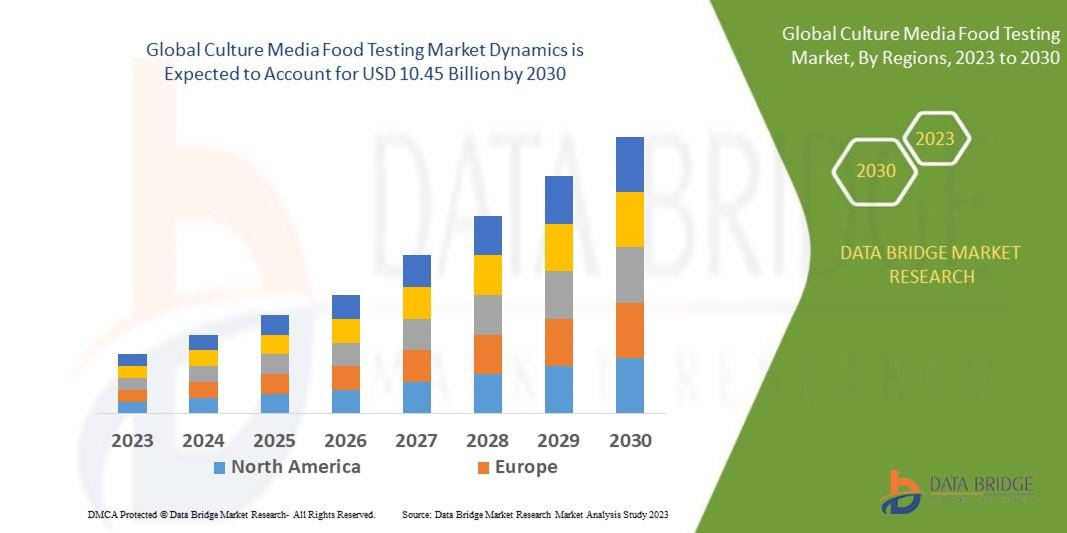

Introduction The Global Culture Media Food Testing Market plays a vital role in ensuring the safety and quality of food consumed worldwide. Culture media serve as essential components in microbiological testing, enabling the detection, isolation, and enumeration of microorganisms in food products. They provide the nutrients necessary for microbial growth and identification, making...

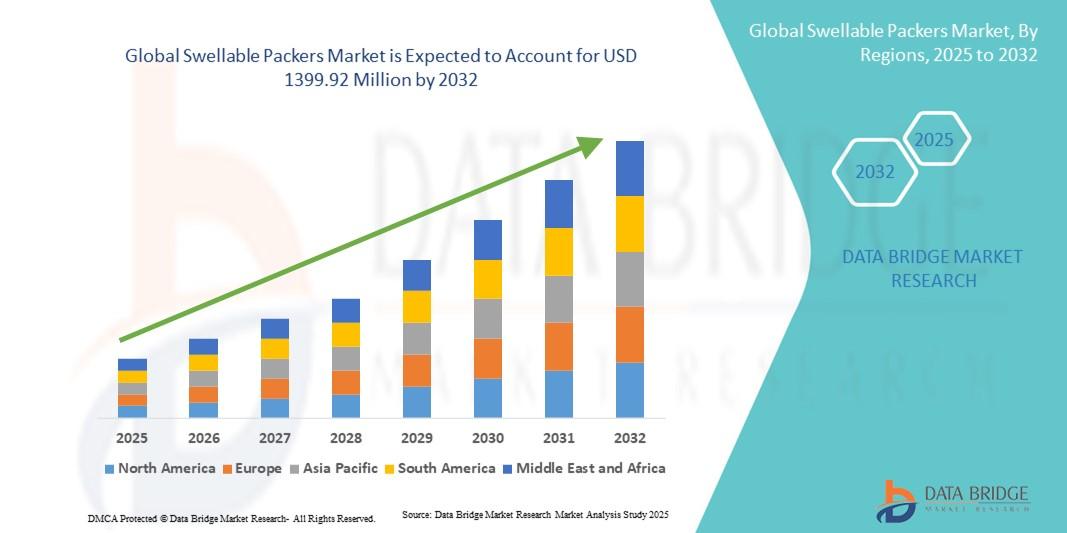

"Future of Executive Summary Swellable Packers Market: Size and Share Dynamics The global swellable packers market size was valued at USD 750.75 million in 2024 and is expected to reach USD 1399.92 million by 2032, at a CAGR of 8.10% during the forecast period Swellable Packers Market research report is a sure solution to get market insights with which business can...

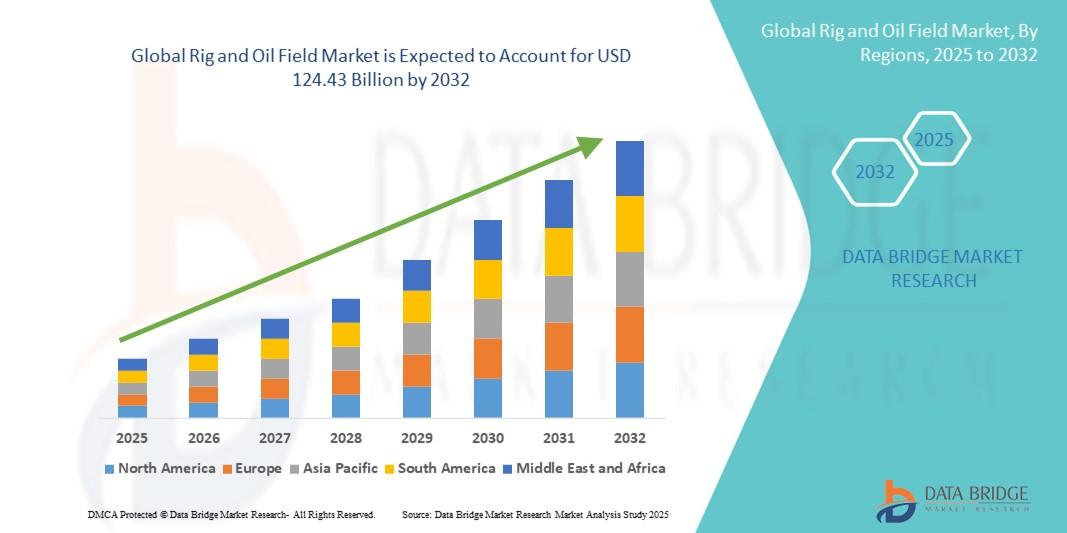

"What’s Fueling Executive Summary Rig and Oil Field Market Size and Share Growth CAGR Value The global rig and oil field market size was valued at USD 75.18 billion in 2024 and is expected to reach USD 124.43 billion by 2032, at a CAGR of 6.50% during the forecast period. An influential Rig and Oil Field Market document supports in achieving a...

The chemical sector remains resurgent, delivering critical inputs in agriculture, healthcare, construction, and consumer uses. With increasing demand for specialty solutions and green products, the sector moves forward incrementally. Growth between 2025 to 2031 will be at a CAGR rate of 4.5% and is strongly connected to the industries in need of safe and secure material innovation. At the core...

The demand for high-performance construction materials has led to the widespread adoption of multi metal aluminum sandwich panels. Their combination of aluminum sheets and insulating cores ensures fire resistance, structural strength, and thermal efficiency. These panels are increasingly used in building facades, cold storage, and industrial applications. Growth in the Multi Metal Aluminum...