Solid-State Battery Market Overview: Growth Drivers and Technological Breakthroughs

Solid-State Battery Market - The Solid-State Battery Market focuses on innovative battery technologies that use solid electrolytes instead of liquid or gel-based ones, offering improved safety, higher energy density, and longer lifespan. Growing adoption in electric vehicles, wearables, and grid storage systems is fueling global market expansion.

The solid-state battery (SSB) market represents a transformative segment within the broader landscape of advanced energy storage solutions. It is characterized by intense research, significant corporate investment, and a competitive race toward commercial viability, poised to reshape industries currently reliant on conventional lithium-ion technology. The core innovation of SSBs lies in replacing the flammable liquid or gel electrolyte used in traditional batteries with a solid counterpart, which fundamentally alters the battery's safety, performance, and design flexibility.

This shift has propelled the market to the forefront of clean energy and electric mobility discussions. The promise of SSBs includes substantial improvements in key performance indicators that are crucial for widespread adoption, particularly in the electric vehicle (EV) sector. By eliminating the liquid component, the risk of thermal runaway, fire, and leakage is drastically reduced, offering an inherently safer battery architecture. This enhanced safety profile is a major qualitative advantage, especially for high-energy applications where public and regulatory scrutiny on battery safety is paramount.

The market's current trajectory is dominated by the pursuit of higher energy density. SSBs hold the potential to utilize a lithium metal anode, which can store significantly more energy than the graphite anodes used in most commercial lithium-ion cells. This technological pathway promises to translate directly into lighter battery packs and, for EVs, a considerable extension of driving range without increasing the vehicle's weight or volume. This singular advantage is a primary driver of market interest from global automotive manufacturers, many of whom have formed strategic alliances or made substantial financial commitments to solid-state battery startups. The automotive application is widely considered the ultimate prize for market dominance due to its massive scale and high-performance demands.

Beyond the automotive sector, the solid-state battery market encompasses a variety of other applications. In consumer electronics, the focus is on achieving thinner, lighter, and safer batteries for devices such as smartphones, wearables, and portable computing. The enhanced design flexibility afforded by solid electrolytes allows for novel form factors, including batteries that can be bent or shaped to fit non-traditional device designs. Furthermore, the longevity and stability of SSBs make them appealing for specialized, high-reliability applications, such as medical devices, aerospace technology, and remote internet-of-things (IoT) sensors, where battery replacement is difficult or safety is absolutely critical.

However, the market is currently navigating significant technical and manufacturing hurdles. The transition from laboratory-scale prototypes to mass production remains the single greatest challenge. Creating a stable and highly conductive interface between the solid electrolyte and the electrodes is notoriously difficult. During charge and discharge cycles, the expansion and contraction of the electrodes can lead to mechanical stress, potentially causing the solid electrolyte to crack or the interface contact to degrade, which results in reduced performance and shorter cycle life. This issue of interfacial stability is a central focus of material science research across the industry.

Another major challenge is the inherent complexity of manufacturing. Unlike the mature, high-volume processes used for liquid lithium-ion batteries, SSBs often require specialized, novel production techniques, such as thin-film deposition or unique sintering processes for ceramic materials. Scaling these complex manufacturing steps while maintaining stringent quality control and achieving a competitive cost structure is a critical barrier to widespread commercialization. Companies are exploring various electrolyte chemistries, including sulfide, oxide, and polymer-based solids, each presenting its own set of production-related complexities and performance trade-offs.

The competitive landscape in the solid-state battery market is fragmented but rapidly consolidating through partnerships. Traditional battery giants, established chemical companies, and cutting-edge startups are all vying for position, often collaborating with major end-users like global automakers. This dynamic interplay of players suggests that the market will evolve through multiple technological pathways before a clear winner or dominant standard emerges. The success of the market ultimately hinges on the ability of these players to resolve the core engineering challenges, prove long-term reliability in real-world conditions, and drastically reduce the cost of production to a point where they can compete effectively with the continually improving performance and established supply chain of conventional lithium-ion batteries. The market's potential for disruptive change is immense, but its realization depends on overcoming these final, persistent engineering and economic obstacles.

Solid-State Battery Market FAQ

What is the fundamental difference that defines a Solid-State Battery Market? The market is defined by batteries that replace the flammable liquid or gel electrolyte of conventional cells with a solid material, which fundamentally alters the cell's safety, energy storage potential, and overall architecture.

Which industry is considered the most significant driver for the adoption of Solid-State Batteries? The electric vehicle industry is widely regarded as the primary driving force, due to the technology's potential for substantial improvements in driving range, safety, and charging speed compared to current battery solutions.

What is the single greatest manufacturing hurdle facing the commercialization of this technology? The most significant hurdle is the challenge of scaling up production from laboratory and prototype levels to high-volume, cost-effective manufacturing while consistently ensuring the long-term stability and integrity of the solid interface between the electrolyte and the electrodes.

More Related Reports:

Categories

Read More

The global Crohn’s Disease Therapeutics Market is witnessing a transformative phase, driven by the rising prevalence of Crohn’s disease and continuous advancements in targeted therapies. Crohn’s disease, a chronic inflammatory bowel disorder, is increasingly affecting populations worldwide, boosting the demand for effective therapeutics. The market is projected to expand...

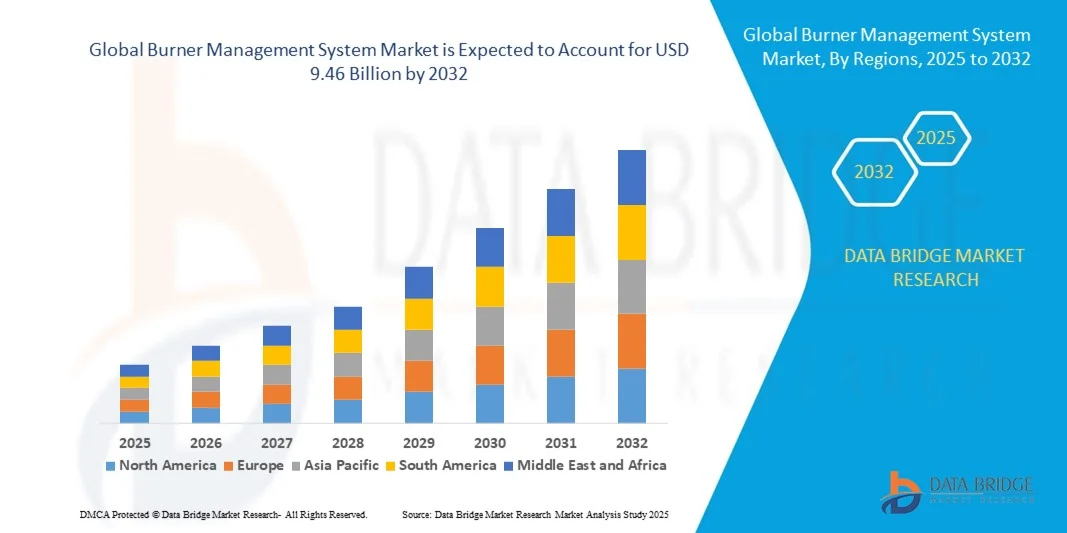

"Executive Summary Burner Management System Market Size and Share Analysis Report The global burner management system market size was valued at USD 5.85 billion in 2024 and is expected to reach USD 9.46 billion by 2032, at a CAGR of 6.20% during the forecast period. Accomplishment of maximum return on investment (ROI) is one of the most wannabe goals for any...

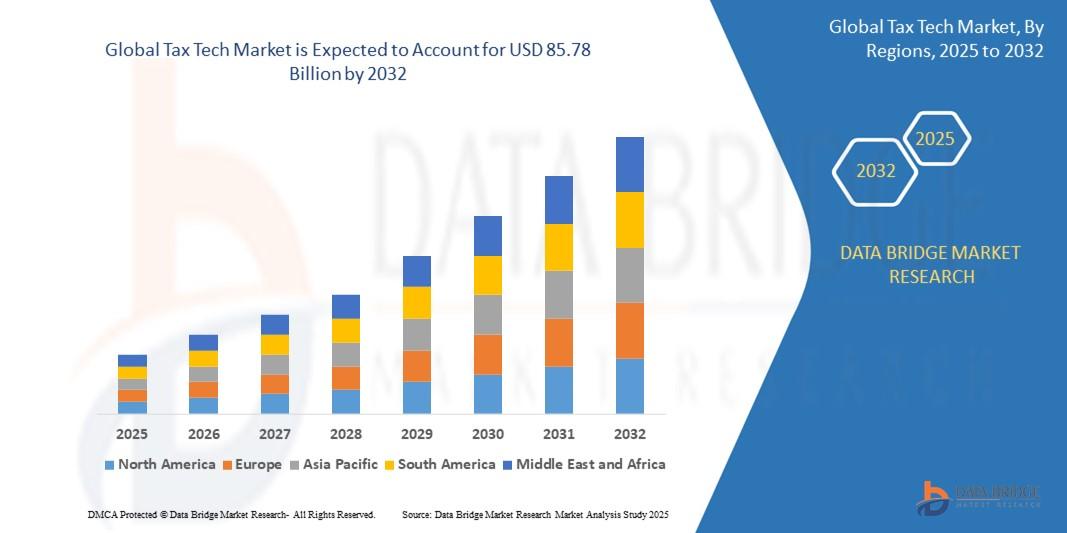

"Competitive Analysis of Executive Summary Tax Tech Market Size and Share CAGR Value The global tax tech market size was valued at USD 34.4 billion in 2024 and is expected to reach USD 85.78 billion by 2032, at a CAGR of 12.10% during the forecast period. To stand apart from the competition, a careful idea about the competitive landscape, their product...

This Feed Additives market report has been prepared by considering several fragments of the present Feed Additives market and upcoming market scenario. The market insights gained through this market research analysis report facilitate a clearer understanding of the market landscape, issues that may interrupt in the future, and ways to position definite brand excellently. It consists...

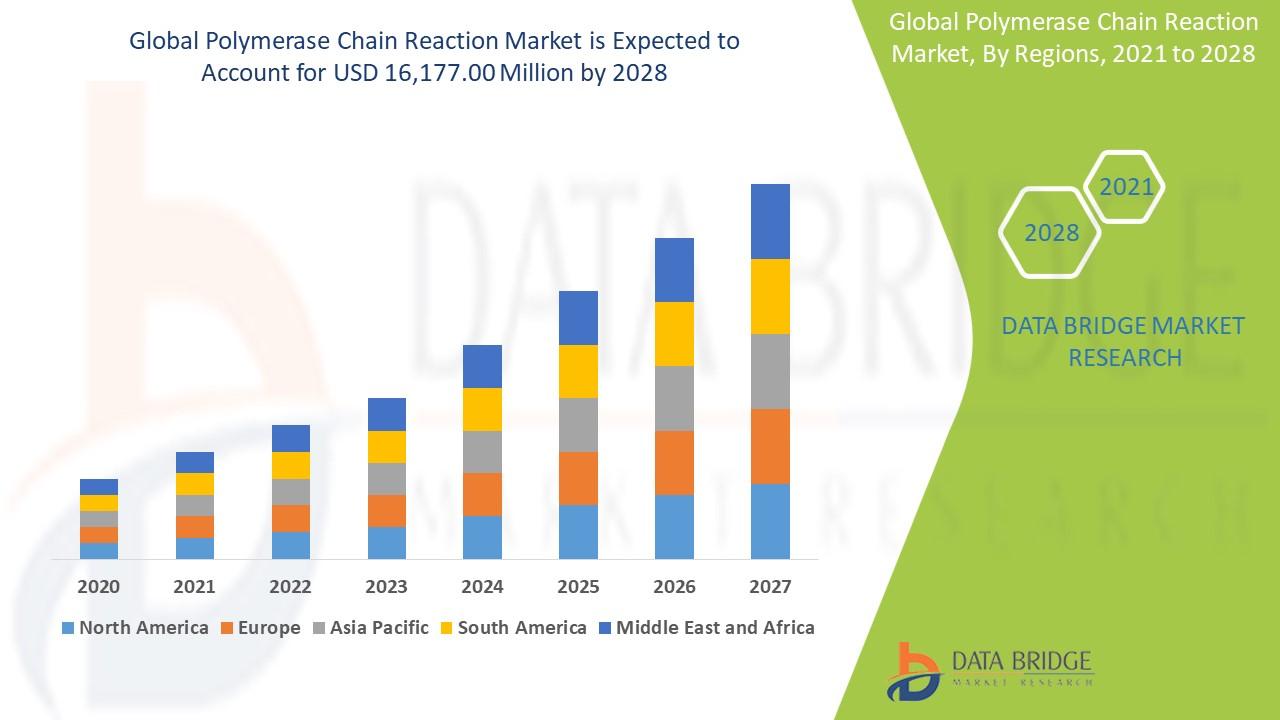

"Executive Summary Polymerase Chain Reaction Market Size and Share Forecast Data Bridge Market Research analyses that the market is growing with the CAGR of 10.4% in the forecast period of 2021 to 2028 and is expected to reach USD 16,177.00 million by 2028. Polymerase Chain Reaction Market business report is a well-generated market report which helps achieve comprehensive analysis of the...